Common Social Security Myths Women Still Believe

The most common Social Security myths women still believe. Clear, honest answers about coverage, timing, and benefits.

What Are the Biggest Social Security Myths Holding Women Back?

The most common Social Security myths aren't dramatic. They're quiet assumptions that shape decisions without women realizing it. Over the years, half-truths and outdated advice have created real confusion around Social Security, especially for women planning retirement. Let's clear up the myths that matter most, because confidence starts with accurate information.

"I can't tell you how many times I've sat with a woman who made her claiming decision based on something a friend told her 10 years ago," says David P. Schaeffer, advisor at American Retirement Advisors. "Getting the facts right on Social Security is worth more than almost any other planning step."

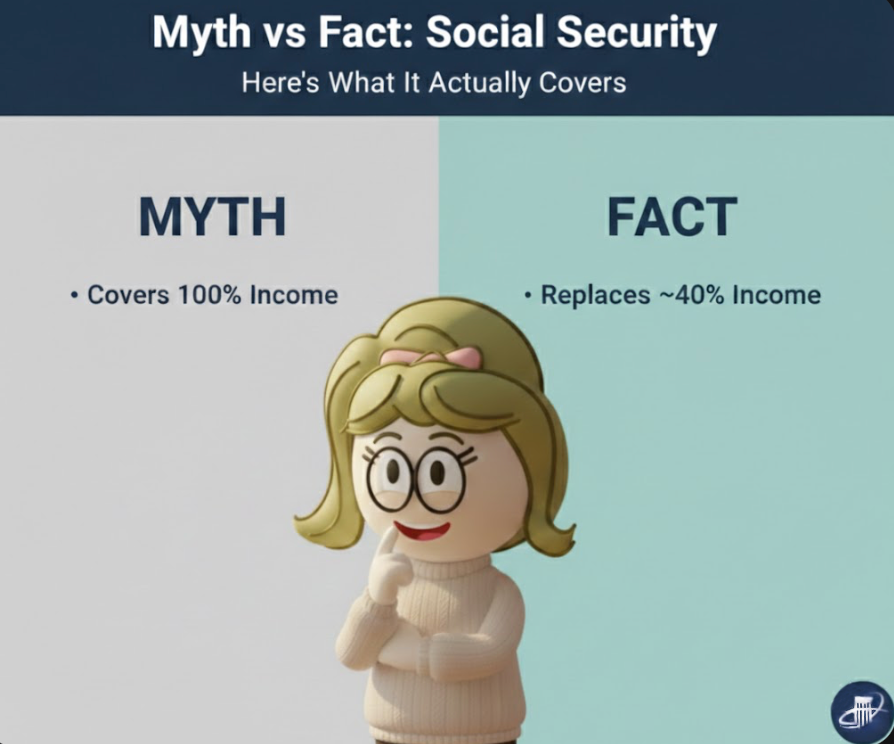

Will Social Security Cover All Your Retirement Expenses?

No. This is the most widespread myth. Many women believe Social Security will replace most or all of their working income. In reality, it was designed to replace roughly 30 to 40 percent of pre-retirement earnings. It's a foundation, not a full replacement. Understanding that lets you plan realistically rather than being surprised later. For a closer look at what Social Security actually provides, read what Social Security really covers.

Is It Always Best to Claim as Early as Possible?

Not necessarily. You can begin at 62, but claiming early permanently reduces your monthly benefit compared to waiting. Early claiming can make sense in certain situations, but it's not automatically the smart move. The right timing depends on your health, income needs, marital status, and long-term plan. There is no one-size-fits-all answer.

Should You Always Wait Until 70 to Claim?

Not always. While waiting increases your monthly benefit, it isn't automatically right for everyone. If you need income sooner or have health concerns, waiting may not provide the advantage you imagine. The key isn't "early" or "late." It's alignment with your overall retirement strategy.

Is Social Security Going to Disappear?

This fear is widespread but not supported by how the program works. While there are ongoing discussions about long-term funding adjustments, Social Security remains a foundational government program. Historically, changes have been gradual, not sudden. Planning should be realistic, not fear-based. Don't make rushed decisions based on headlines. For the latest policy updates, see the Social Security Fairness Act and what it means for retirees, and for a deeper understanding of the system, read understanding and maximizing Social Security.

Does Divorce Eliminate Your Social Security Options?

No. If you were married for at least 10 years and haven't remarried, you may be eligible for benefits based on your ex-spouse's earnings record. This doesn't reduce their benefit. It's a separate entitlement that many divorced women don't know they have. Don't leave money on the table because of a myth.

Frequently Asked Questions

Does working after claiming Social Security reduce my benefit?

Only if you're under full retirement age. Before FRA, earning above a certain threshold temporarily reduces your benefit. But this isn't lost money. Social Security recalculates your benefit at FRA to credit you for the months benefits were reduced. After full retirement age, you can earn any amount without reduction.

Can I collect Social Security based on my spouse's earnings?

Yes. If your spouse's benefit is higher, you may be eligible for a spousal benefit of up to 50% of their full retirement age amount. This is available even if you have your own work record. You'll receive whichever amount is higher, your own benefit or the spousal benefit.

Will my Social Security benefit keep up with inflation?

Social Security includes annual cost-of-living adjustments (COLAs) based on the Consumer Price Index. While COLAs help, they don't always fully match the real increase in expenses like healthcare and housing. That's why having income beyond Social Security is important for long-term purchasing power.

Betty's Bottom Line

Social Security myths are quiet, but they shape real decisions. The truth is simpler than most women expect: Social Security is a strong foundation, timing is personal, the program isn't disappearing, and divorced women may have options they don't know about. Get the facts right, and everything else in your retirement plan becomes clearer.

Save This to Pinterest