Planning Doesn't Mean Something Is Wrong

Planning doesn't mean something is wrong. It's a confidence habit, not a warning sign.

Why Do Some Women Avoid Retirement Planning?

Because they quietly believe that reviewing their finances means something must be wrong. There's a quiet belief many women carry: "If I start looking too closely, it must mean there's a problem." But planning isn't a reaction to danger. It's a habit of confidence. Reviewing your retirement income, organizing documents, and asking questions aren't signs of fear. They're signs of responsibility.

"The women who plan regularly are also the calmest," says David P. Schaeffer, advisor at American Retirement Advisors. "Not because everything is perfect, but because they always know where they stand."

Don't We Plan for Everything Else Without Worry?

Think about how naturally you plan in other areas of life. Vacations, holidays, meals for the week. Planning doesn't mean you expect something to go wrong. It means you want things to go smoothly. Retirement planning is no different. It's not about bracing for disaster. It's about creating steadiness.

Is Avoiding Your Finances Actually Easier?

It feels easier, but it's heavier. Avoidance doesn't remove uncertainty. It quietly increases it. A calm review, even once or twice a year, often brings relief. Because most of the time, things aren't as uncertain as they feel. And if adjustments are needed, they're usually manageable. For more on building this confidence habit, read it's okay to ask for help with money.

What Happens When You Start Planning Regularly?

The irony is this: women who plan regularly tend to feel less anxious, not more. They don't carry a mental cloud of "I hope everything is fine." They know. They've looked. They've asked questions. They've adjusted. That's what confidence is made of. Not certainty, but informed awareness. For a helpful starting point, read you're not behind, you're preparing.

What Is the Simplest Way to Start?

Choose one small action. Look at your retirement account balance. Review one beneficiary form. Write down one question for your advisor. You don't need a complete financial overhaul. You need five minutes of attention. That's enough to break the avoidance cycle and start building the habit of awareness. For professional guidance, the ARA team explains why personal service matters in retirement planning and has a reassuring piece about getting ready at any stage.

Frequently Asked Questions

How often should I review my retirement plan?

At least twice a year, or whenever a major life event occurs (marriage, divorce, health change, job change). A brief review takes 30-60 minutes and usually brings more relief than stress. The goal is awareness, not perfection.

What if reviewing my finances makes me more anxious?

That anxiety usually fades once you see the actual numbers. Most women find that reality is less scary than the uncertainty. If looking at your finances feels overwhelming, consider doing it with an advisor who can provide context and reassurance alongside the numbers.

Do I need a financial advisor to do a retirement review?

You can start on your own by reviewing account balances, expenses, and beneficiary forms. But a professional review adds significant value: they can identify gaps, optimize your strategy, and stress-test your plan against different scenarios. Most advisors offer an initial consultation at no cost.

Betty's Bottom Line

Planning doesn't mean something is wrong. It means you're taking ownership of your future. The women who plan regularly are the ones who sleep best at night. Not because everything is perfect, but because they know where they stand. Start with one small action this week. That's all it takes to shift from avoidance to awareness.

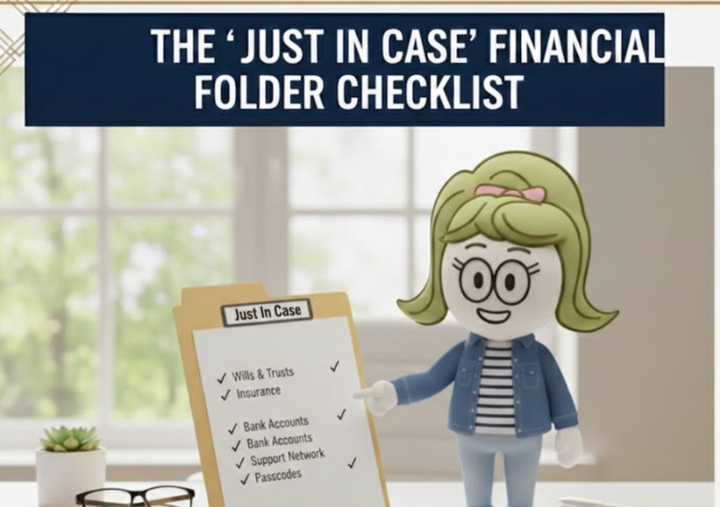

Save This to Pinterest