What Women Don't Realize Until They're Suddenly Alone

What women don't realize until they're suddenly alone. How income changes and what you can do now to prepare.

What Financial Changes Catch Women Off Guard When They're Suddenly Alone?

The biggest surprise isn't emotional. It's financial. Many women eventually find themselves managing retirement alone, whether through widowhood, divorce, or simply outliving their partner. What makes that transition difficult isn't only the loss. It's the financial shift that follows, and most women don't realize what changes until they're already in it.

"The women who navigate this transition best are the ones who understood the financial picture before they needed to," says David P. Schaeffer, advisor at American Retirement Advisors. "Not every detail, just the big pieces: where the income comes from, where the accounts are, and who to call."

What Happens When Two Incomes Become One?

When both spouses receive retirement income, it feels stable. Two Social Security checks. Two retirement accounts. Shared expenses. But when one spouse passes, household income usually decreases. The surviving spouse receives the higher of the two Social Security benefits, not both. That can mean a noticeable reduction in monthly income while most household expenses stay the same. The mortgage doesn't shrink. Utilities don't cut in half. Property taxes stay steady. This is one of the first surprises women face.

Why Do Financial Responsibilities Shift So Quickly?

In many marriages, one partner handles most of the financial details. Paying bills, managing investments, tracking withdrawals. When that partner is gone, the surviving spouse suddenly faces decisions she didn't previously manage. Not because she isn't capable, but because she wasn't regularly handling those tasks. Preparedness isn't about expecting loss. It's about making sure both partners understand the financial picture while things are calm. For practical steps, read the widow preparedness starter guide.

How Does Being Alone Change How Investments Feel?

When you're managing finances alone, risk feels different. Market fluctuations that once felt manageable may suddenly feel threatening. Without a partner to discuss decisions with, investment choices can feel heavier. This doesn't mean you need to change everything. It means your strategy may need to adjust to reflect your comfort level and your new income needs. A trusted advisor can help you find the right balance between growth and security.

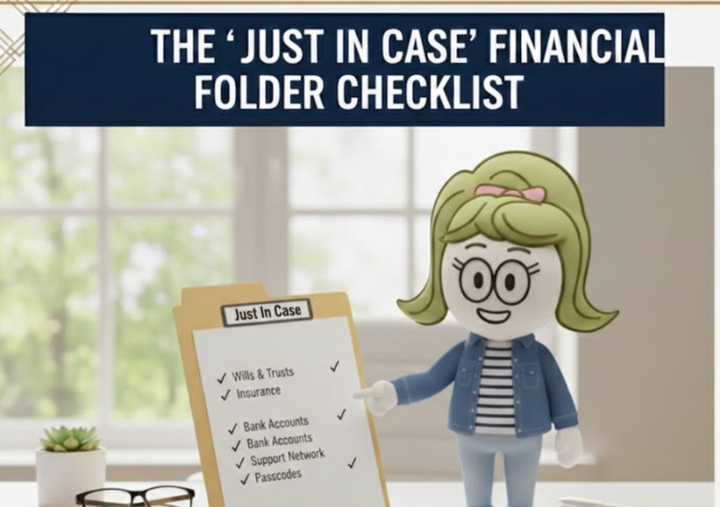

What Can You Do Right Now to Prepare?

You don't have to wait for something to happen. Start by knowing where your accounts are, understanding how income would change, organizing key documents, and identifying a professional you'd call if you needed help. These steps take less time than you'd think, and the peace of mind they create is enormous. For a helpful perspective on grief and finances, the ARA team wrote thoughtfully about how loss affects well-being, and their guide on the emergency document box is a practical place to start.

Frequently Asked Questions

How much does household income typically decrease when a spouse passes?

It varies, but many widows see a 30 to 50 percent reduction in total household income. The surviving spouse keeps the higher of the two Social Security benefits while the other stops. Pension income may also change depending on the plan's survivor options. Understanding these numbers before they become reality helps prevent financial shock during an already emotional time.

What is the first financial step a widow should take?

Contact Social Security to report the passing and apply for survivor benefits. Then review all income sources, check beneficiary designations on every account, and locate important documents. Avoid making major financial decisions in the first few months. Focus on stability first, strategy later.

How can married women prepare financially for the possibility of being alone?

Make sure both partners know where all accounts are, understand how income would change, and have access to important documents. Review beneficiary designations annually. Have honest conversations about what the financial picture looks like if one spouse passes first. These steps take minutes but can prevent months of confusion.

Betty's Bottom Line

The financial shift that comes with being suddenly alone catches most women off guard, not because they aren't capable, but because they weren't informed. Knowing where your income comes from, where your accounts are, and who to call doesn't take long to figure out. Do it while things are calm, not while you're grieving. That's one of the strongest things you can do for yourself.

Save This to Pinterest